Recent Posts

categories

Archives

- Tips to Lower your Electric BillPosted: 4 years ago

- 5 Easy Home Improvement Projects & Upgrades For the WinterPosted: 4 years ago

- Benefits to buying in the winterPosted: 4 years ago

- Cash In with a Cash-Out RefinancePosted: 5 years ago

- Mortgage MythsPosted: 5 years ago

- Q&A: All About Flooring — Hardwood, Carpeting, Tiling, LaminatePosted: 5 years ago

- Tip: 3 Foolproof Social Media Marketing TipsPosted: 5 years ago

- Tips for Hosting a Stress-Free Holiday DinnerPosted: 5 years ago

- Is a Mortgage Refinance Right for You?Posted: 6 years ago

- Check Your Disaster Supplies KitPosted: 6 years ago

- Create an Early Holiday Shopping BudgetPosted: 6 years ago

- 9 Ways to Make Moving Day EasierPosted: 6 years ago

- July 2018 Market Update – Twins Cities RegionPosted: 6 years ago

- Fall Homeowners ChecklistPosted: 6 years ago

- Scam Alert: Spoofed IRS Phone NumbersPosted: 6 years ago

- 15 Years of First Class MortgagePosted: 6 years ago

- How to buy a second homePosted: 6 years ago

- Q&A: Lawn Watering SecretsPosted: 6 years ago

- Troubleshoot Your Air ConditioningPosted: 6 years ago

- Your Mortgage, What to Expect: Clear To ClosePosted: 6 years ago

- Twins Cities Region Monthly Indicators – APRIL 2018Posted: 6 years ago

- Your Mortgage, What to Expect: UnderwritingPosted: 6 years ago

- Your Mortgage, What To Expect: Property AppraisalPosted: 6 years ago

- 3 Tips to Improve your Credit Score and Score a Lower Interest RatePosted: 6 years ago

- Changing Interest Rates Have A High Impact On Purchasing PowerPosted: 6 years ago

- The Myth of Multiple Mortgage Credit InquiriesPosted: 6 years ago

- Things to do BEFORE you buy a home.Posted: 6 years ago

- March Tech Tip: Pack Smarter With PackPointPosted: 6 years ago

- 4 Ways to Pay Off Your Mortgage EarlyPosted: 6 years ago

- Clean House in a HurryPosted: 6 years ago

- Your Mortgage, What To Expect: Document ReviewPosted: 6 years ago

- Chill Winter Utility BillsPosted: 6 years ago

- Six Tips to Help Your Home Sell This FallPosted: 7 years ago

- 4 Things to Know About Closing CostsPosted: 7 years ago

- Understanding Your Credit ScorePosted: 7 years ago

- Equifax Data Breach: What should you do now?Posted: 7 years ago

- Should You Refinance Your FHA to a Conventional Loan?Posted: 7 years ago

- 6 Ways to Save on Paint ProjectsPosted: 7 years ago

- Q&A: Mortgage InsurancePosted: 7 years ago

- How to Keep Your House Cool this SummerPosted: 7 years ago

- Mortgage Education: “What’s the Point?”Posted: 7 years ago

- Q&A: Spotting a Spoof SitePosted: 7 years ago

- Moving ChecklistPosted: 7 years ago

- Squash Marital Money SquabblesPosted: 7 years ago

- April 2017: Twin Cities Real Estate Market UpdatePosted: 7 years ago

- Your Spring Guide to Home StagingPosted: 7 years ago

- March 2017: Twin Cities Real Estate Market UpdatePosted: 7 years ago

- Don’t be a Victim — Four Ways Protect Yourself from Refinance ScamsPosted: 7 years ago

- Local Market Update: Minneapolis Area Association of RealtorsPosted: 7 years ago

- First-Time Homebuyers: Where to startPosted: 7 years ago

- Dear First Class Mortgage:Posted: 7 years ago

- First Class Mortgage. Our Expertise, Your Peace of Mind.Posted: 7 years ago

21

May

3 Tips to Improve your Credit Score and Score a Lower Interest Rate

Posted by A good credit score translates into lower interest rates. In a mortgage lender’s eyes, the higher your score is, the less risk you are, and the more likely it is you will pay off your debt. For this reason, borrowers with lower scores can end up paying higher interest rates on their loans.

A good credit score translates into lower interest rates. In a mortgage lender’s eyes, the higher your score is, the less risk you are, and the more likely it is you will pay off your debt. For this reason, borrowers with lower scores can end up paying higher interest rates on their loans.

If this is you, don’t panic!

There are some things you can do to adjust your credit score to receive a favorable review from the underwriter. Here are a few suggestions:

#1: Pay your bills on time:

The simplest, and sometimes hardest, thing you can do is pay all your bills on time. Generally, you can improve your scores by making all your payments on time, keeping debt levels low (below 30%, and ideally 10% of available credit), removing errors and limiting credit inquiries.

If you are still treating your personal financing like you are a struggling college student, it is time to start #adulting. If you do, your credit score will start climbing.

#2: Keep existing credit card accounts open

Part of your credit score is based on credit history. If you have old credit cards that you don’t use very much, you still have the benefit of the credit history they represent.

Rather than trying to pay off all your credit cards, you can move part of the debt from one card to another to even out the distribution of debt. Try to keep balances as close to zero as possible, and definitely below 30% of the available credit limit when trying to purchase a home. Also, if your credit provider will increase your line of credit, the ratio of debt to available credit is automatically reduced.

#3: Fix errors on your credit report

If you are not already doing so, pull a FREE credit report annually. If items are showing up on your credit report that you know you have already paid, request to have the credit bureau remove them. They are obligated to rectify this within 30 days.

If there are items on your credit report that are less than two years old, send in your payment if possible and mark the back of the check with the following notation: “Accepting this check is evidence that the transaction is complete, and this charge will be deleted from my credit record.” If necessary, the canceled check will be proof that this should be promptly removed from your credit report if it interferes with the closing of your loan.

If you are still not sure of what step to take to secure yourself a low-interest rate, contact our team of mortgage professionals to schedule a time to review your financial situation. The appointment is FREE and no-commitment.

03

August

Should You Refinance Your FHA to a Conventional Loan?

Posted by

If you are like most first-time homeowners, your first mortgage was an FHA loan. Your FHA loan gave you the ability obtain financing, requiring only minimal down payments and fair-to-good credit scores. While this was a perfect fit for you at the time, you now may be looking to save some money. One way to do this is to refinance into a conventional loan.

One significant advantage of switching to a conventional loan is that, with the right loan-to-value ratio, it can eliminate mortgage insurance. While conventional loans have stricter credit requirements, and typically require borrowers to have at least 20% equity in their homes, any mortgage insurance provision cancels once your house reaches a 78% loan-to-value ratio.

Additionally, refinancing to a conventional mortgage may allow you to take out a larger home loan.

Refinancing does come with costs, such as closing fees, and may require you to present many of the same documents during the application process as you did with your original home purchase. Plus, you may also need to pay for an appraisal of your home.

Checklist: When Is a Good time to Refinance from an FHA to a Conventional Mortgage?

If you’re still not sure whether you should refinance from an FHA loan into a conventional mortgage? Take a couple of minutes to answer the following questions. They can help you decide if a refinance is right for you.

1. What are my goals?

2. Does refinancing make financial sense?

3. What is the current value of my home?

4. What is my existing home equity?

5. Can I afford the refinancing closing costs and fees?

6. Can I provide all of the necessary documentation?

Considering a Refi? Let us help!

Our expert mortgage consultants can help you evaluate your current loan situation and help you identify if a refinance is right for you. Give us a call today!

Source: PennyMac, Link

09

June

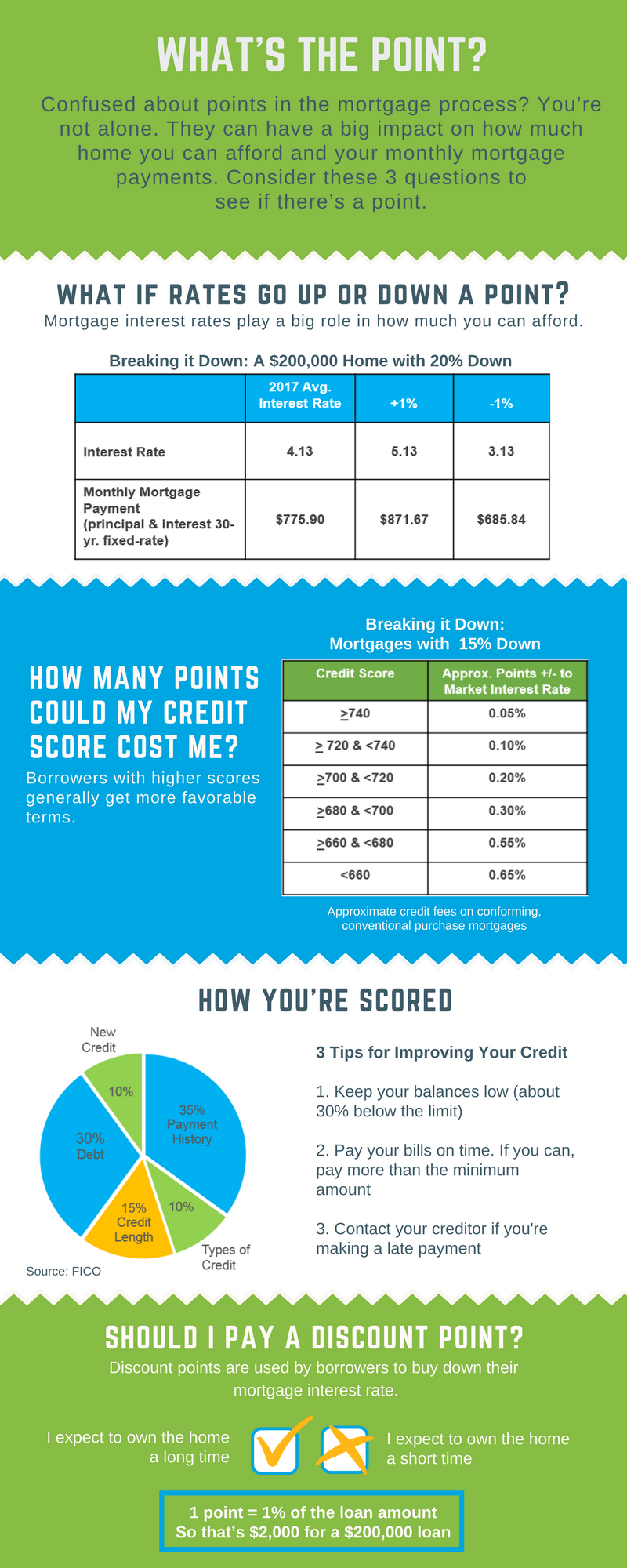

Mortgage Education: “What’s the Point?”

Posted by For a lot of homebuyers, there is a steep learning curve when purchasing a home. When it comes to getting a mortgage, it may feel like you are learning a whole new language.

For a lot of homebuyers, there is a steep learning curve when purchasing a home. When it comes to getting a mortgage, it may feel like you are learning a whole new language.

One of the terms that cause a lot of confusion with homebuyers is “Points.”

Freddie Mac created an easy to use infographic that considers three important questions — interest rate points, credit rate points and discount points — to help you and your clients get the point on points.

CLICK HERE FOR FULL INFOGRAPHIC

Remember, everyone’s situation is different so give us a call today to see what’s best for you.

Source: Freddie Mac, Link

17

April

March 2017: Twin Cities Real Estate Market Update

Posted by We can comfortably consider the first quarter to have been a good start for residential real estate in 2017.

We can comfortably consider the first quarter to have been a good start for residential real estate in 2017.

There was certainly plenty to worry over when the year began. Aside from new national leadership in Washington, DC, and the policy shifts that can occur during such transitions, there was also the matter of continuous low housing supply, steadily rising mortgage rates and ever-increasing home prices. Nevertheless, sales have held their own in year-over-year comparisons and should improve during the busiest months of the real estate sales cycle.

New Listings in the Twin Cities region increased 1.3 percent to 8,032. Pending Sales were down 3.0 percent to 5,631. Inventory levels fell 19.9 percent to 10,213 units.

Prices continued to gain traction. The Median Sales Price increased 7.0 percent to $237,500. Days on Market was down 14.1 percent to 73 days. Sellers were encouraged as Months Supply of Homes for Sale was down 23.1 percent to 2.0 months.

The U.S. economy has improved for several quarters in a row, which has helped wage growth and retail consumption increase in year-over-year comparisons. Couple that with an unemployment rate that has been holding steady or dropping both nationally and in many localities, and consumer confidence is on the rise. As the economy improves, home sales tend to go up. It isn’t much more complex than that right now. Rising mortgage rates could slow growth eventually, but rate increases are little more than a byproduct of the strong economy and high demand.

Source: Minneapolis Area Association of Realtors®, Monthly Indicators Report. All data comes from NorthstarMLS. http://maar.stats.10kresearch.com/reports

08

March

Local Market Update: Minneapolis Area Association of Realtors

Posted by Twin Cities — (January 2017) January brings out a rejuvenated crop of buyers with a renewed enthusiasm in a new calendar year. Sales totals may still inevitably start slow in the first half of the year due to ongoing inventory concerns. Continued declines in the number of homes available for sale may push out potential buyers who simply cannot compete for homes selling at higher price points in a low number of days, especially if mortgage rates continue to increase.

Twin Cities — (January 2017) January brings out a rejuvenated crop of buyers with a renewed enthusiasm in a new calendar year. Sales totals may still inevitably start slow in the first half of the year due to ongoing inventory concerns. Continued declines in the number of homes available for sale may push out potential buyers who simply cannot compete for homes selling at higher price points in a low number of days, especially if mortgage rates continue to increase.

New Listings in the Twin Cities region increased 3.1 percent to 4,304. Pending Sales were up 4.3 percent to 3,130. Inventory levels fell 25.4 percent to 8,212 units.

Prices continued to gain traction. The Median Sales Price increased 4.7 percent to $225,000. Days on Market was down 7.1 percent to 79 days. Sellers were encouraged as Months Supply of Homes for Sale was down 30.4 percent to 1.6 months.

In case you missed it, we have a new U.S. president. In his first hour in office, the .25 percentage point rate cut on mortgage insurance premiums for loans backed by the Federal Housing Administration (FHA) was removed, setting the table for what should be an interesting presidential term for real estate policy. FHA loans tend to be a favorable option for those with limited financial resources.

On a brighter note, wages are on the uptick for many Americans, while unemployment rates have remained stable and relatively unchanged for several months. The system is ripe for more home purchasing if there are more homes available to sell.

Source: Minneapolis Area Association of Realtors®, Monthly Indicators Report. All data comes from NorthstarMLS. http://maar.stats.10kresearch.com/reports

Mortgage Services

Tools

About Us